Entering a bank to request a loan feels like a straightforward transaction, but beneath the surface lies a complex world of percentages and timelines. Most borrowers focus solely on whether they can afford the monthly check, yet understanding how to calculate loan interest is the single most important factor in determining your long-term wealth. In my experience, a borrower who understands the math is a borrower who keeps their money; those who don’t end up funding the bank’s next skyscraper.

The Illusion of the “Simple” Loan

There is a common financial myth that “just a small interest rate” won’t hurt your bottom line. I’ve observed that many people treat an 8% interest rate as a flat fee. In reality, interest is a living, breathing cost that grows over time.

The high cost of financial illiteracy in today’s high-interest world is staggering. If you don’t know the difference between a flat rate and a reducing balance, you are essentially flying blind. From working with clients, I’ve seen how a mere 1% misunderstanding in a mortgage rate can cost a family three to five years of their total household income over the life of a 30-year loan.

Decoding the DNA of Your Debt

To master your finances, you must first understand the three pillars of any loan:

- The Principal: This is more than just the “sticker price” of your car or home. It is the core debt upon which all interest is built.

- The Rate: This is where it gets tricky. In practice, there is a massive difference between the nominal rate and the APR (Annual Percentage Rate). The APR includes fees and costs that the nominal rate hides.

- The Tenure: Think of tenure as the silent multiplier. The longer you take to pay back the principal, the more opportunities the interest has to compound and grow.

Simple vs. Compound Interest: The Power of Frequency

Breaking down the math reveals a stark truth: interest can either be your greatest tool (in savings) or your heaviest burden (in debt). Simple interest is calculated only on the principal, but most modern bank loans utilize compounding or reducing balance methods.

How compounding intervals change your monthly obligation is often overlooked. Whether interest is calculated monthly, quarterly, or annually changes the “Effective Interest Rate.” Furthermore, you must face the “Amortization” Reality. In the early years of a loan, the vast majority of your payment goes toward interest, not the principal. This is why your balance barely moves in the first few years of a mortgage.

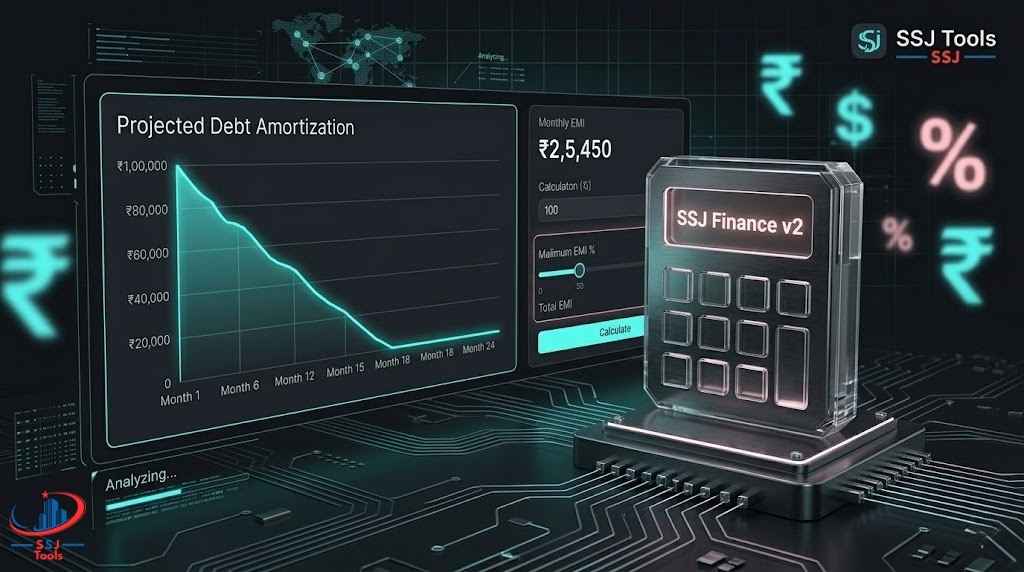

Manual Math vs. The SSJ Finance Engine

You could try to calculate these figures using a pen, paper, and long-form algebraic equations, but the risk factor is high. A single human error in a spreadsheet formula can lead to miscalculated budgets and, eventually, late fees or defaults.

This is what is a loan calculator designed for: to remove the margin of error. Moving from manual formulas to the instant precision of an interest calculator ensures that you are seeing the true cost of debt. The SSJ Finance v2 is specifically engineered to prevent “Calculation Fatigue.” Instead of wrestling with decimals, you get a clean, instant breakdown of your liability.

Expert Workflow: Visualizing Your Debt with SSJ Tools

When I consult on debt management, I follow a specific four-step workflow using the SSJ Finance Engine:

- Step 1: Establishing your baseline principal: Input the exact amount you intend to borrow.

- Step 2: Stress-testing scenarios: Don’t just check one rate. Input a rate 0.5% higher and 0.5% lower to see how the numbers shift.

- Step 3: Analyzing the Amortization Calculator: Look at the “Total Interest Payable” figure. If that number shocks you, your tenure is too long.

- Step 4: Exporting your Action Plan: Use these precise figures to negotiate with your bank. When you show a lender you know the exact math, they are less likely to pad your loan with “fluff” fees.

Common Pitfalls in Loan Planning

The most dangerous trap is the “Low Monthly Payment” Trap. Lenders often offer to lower your monthly EMI by extending the tenure. While this feels like “breathing room,” you are actually trading a lower monthly payment for infinite interest costs over time.

Additionally, many users ignore the “Total Repayment” figure. They focus on the ₹20,000 a month but ignore the fact that they are paying back ₹15 Lakhs on a ₹10 Lakh loan. Finally, never mistake a simple loan calculator result for a final binding offer; always use it as a benchmark to verify the bank’s paperwork.

Best Practices for Savvy Borrowers

From my real-world experience, the best strategy is the “Tenure Reduction” strategy. If you can afford to pay even 10% more than your calculated EMI, you can shave years off your debt.

I always recommend checking the SSJ Finance Engine before you even step foot in a dealership or a bank. By leveraging instant feedback loops, you can find your “sweet spot”—the perfect balance where the EMI is affordable, but the total interest paid is kept to a minimum.

FAQ: Common Borrowing Questions

How does a loan calculator work differently than a standard calculator?

A standard calculator does basic arithmetic. A loan calculator uses a specific amortization formula to account for the declining principal balance and the time-value of money.

What is the mathematical difference between flat and reducing rates?

A flat rate calculates interest on the original principal for the whole term. A reducing rate (used by SSJ Tools) calculates interest only on the remaining balance, which is almost always cheaper for the borrower.

What exactly is an amortization schedule, and why should I care?

It is a table showing every payment of the loan. You should care because it shows you exactly when you will start making a “dent” in the actual principal rather than just paying off interest.

Is it better to focus on the monthly payment or the total interest paid?

While the monthly payment must fit your budget, the total interest paid is the true “price” of the loan. A savvy borrower optimizes for the lowest total interest.